Technology news, told as a power drama.

Editor’s note:

Silicon Drama is eTatos.com’s weekly series about the battle for AI, compute, chips, agents and robots. The goal is simple: Not just to report what happened, but to explain why it matters, who gains power, who loses control and where the next conflict is already forming.

SpaceX went public.

That sentence alone would have been enough for a normal tech week.

But this was not a normal tech week.

SpaceX raised $75 billion in the largest IPO in history. Elon Musk crossed the trillion-dollar line. States challenged index providers over how fast SpaceX could be pushed into major benchmarks. OpenAI and Anthropic moved closer to Wall Street. Claude Fable 5 triggered a trust crisis. Agents got cloud workspaces, schedules, credentials and payment rails. The power grid became a strategic character. Robots moved from demo videos into industrial plans.

This week, the model race had turned into a battle over the full stack of intelligence.

The satellite above Earth.

The data center outside town.

The chip fab in Taiwan.

The agent inside the cloud workspace.

The wallet connected to the workflow.

The robot on the factory floor.

The pension fund pulled into the index.

Every layer had an owner, a bill, a risk and a gatekeeper.

Compute needed capital.

Agents needed credentials.

Payments needed rails.

Robots needed factories.

Data centers needed power.

Chips needed water.

Trust needed daylight.

And underneath all of it sat the question that defined the week:

Once intelligence becomes infrastructure, who gets to own it?

Act I: SpaceX rings the bell for the AI empire

SpaceX priced its IPO at $135 per share, raised $75 billion and reached a valuation of roughly $1.77 trillion.

That kind of number does something strange to a story.

It turns engineering into mythology.

Rockets become balance-sheet items.

Satellites become public-market promises.

Orbit becomes a growth strategy.

AI compute becomes part of the pitch.

SpaceX entered the market like a rocket launch with a ticker symbol.

The company sold more than Starlink, more than launch dominance, more than Mars. It sold a vision in which AI infrastructure eventually leaves the ground.

The AI1 satellite concept gave the week its most cinematic image: A solar-powered compute platform in orbit, using technology SpaceX says can borrow from Starlink V3, producing around 120 kilowatts of sustained compute power and peaking near 150 kilowatts.

A data center above Earth.

No local community fighting over land use.

No town hall meeting about power prices.

No cooling tower on the horizon.

Just sunlight, radiators, laser links and chips.

Of course, the spreadsheet still has to meet physics. The orbital data-center dream may take longer, cost more, or disappoint investors who confuse a presentation slide with infrastructure. Space has a habit of punishing confidence.

But markets do not wait for engineering certainty.

They buy the story early, then ask reality to catch up.

This week, Wall Street bought the sky.

Act II: The first trillionaire

The IPO pushed Elon Musk into a place no individual had reached before.

Trillionaire.

The word feels too large to behave like normal language. It sounds fictional, almost vulgar, a number from a sci-fi novel where one founder controls rockets, cars, satellites, tunnels, AI labs, brain interfaces and a social network.

Now it has a market close.

Musk’s SpaceX stake became worth hundreds of billions on its own. His total net worth moved above the trillion-dollar line. One person became the human logo for an entire age: Space, AI, compute, politics, retail investor belief and extreme capital concentration wrapped into one public-market event.

This is the Muskonomy.

A gravitational field where companies, investors, governments, fans, critics, journalists and regulators keep circling the same name.

The SpaceX IPO was so large that even index rules started to move around it.

Investment officials from several U.S. states challenged Nasdaq and FTSE Russell over possible fast-track treatment for SpaceX. Their concern was practical: If SpaceX enters major indexes too quickly, pension funds and passive investors may be pulled into a huge, tightly controlled company before the market fully understands the risks.

That was the financial scene of the week.

Not the opening bell.

Not the celebration.

Not the trillionaire headline.

The pension fund.

Because that is where the AI infrastructure boom becomes intimate. It leaves the keynote stage and enters retirement accounts.

Some investors will actively choose the SpaceX story.

Others may simply wake up owning a piece of it through an index.

Act III: Sam and Dario take the war public

While Musk owned the market spectacle, another rivalry sharpened.

OpenAI and Anthropic spent the week looking less like research labs and more like rival dynasties preparing for public life.

Reuters framed the fight as a bitter battle for the future of AI. It fits.

The split began inside OpenAI, when Dario Amodei and others left over scaling, safety and trust. That internal fracture now shapes the industry.

Sam Altman versus Dario Amodei.

Speed against restraint.

Distribution against control.

The superapp against the guarded model.

Wall Street charm against safety alarm.

OpenAI against Anthropic.

Both companies now move toward the same financial stage.

OpenAI filed confidential IPO paperwork. Anthropic did the same. Each wants more capital, more infrastructure, more enterprise customers, more influence and a stronger claim on the future.

The public arguments differ.

The capital needs look familiar.

OpenAI published its plan for a third phase of the company.

The first phase was research.

The second was ChatGPT.

The third is an attempt to make powerful AI abundant, useful and cheap enough to touch everything.

The sharpest line was not the marketing language. It was the prediction.

By March 2028, OpenAI expects AI systems to do a significant share of OpenAI’s own research alongside human researchers.

That is the moment the story turns inward.

OpenAI is preparing for AI that helps build the next AI.

Anthropic is telling a similar story in a darker key. Dario Amodei published a policy essay comparing Washington to Treebeard from The Lord of the Rings: Wise, slow, ancient and perhaps too late.

He wants faster regulation, stronger evaluations, chip export controls, possible slowdowns for risky frontier systems and a government that can move before exponential curves make politics irrelevant.

The contradiction is hard to miss.

Anthropic is racing.

Anthropic is warning.

Anthropic is building the machine.

Anthropic is asking for a brake.

That tension may define the next phase of AI better than any benchmark.

Act IV: Claude Fable 5 breaks trust before it breaks records

Then Claude Fable 5 arrived.

Anthropic released Fable 5 as a public Mythos-class model, with Mythos 5 reserved for selected partners and defensive cyber use cases. Same underlying model. Different access. Different safeguards.

On paper, the strategy made sense.

Give the market a powerful model.

Keep the more dangerous capabilities under tighter control.

Push Anthropic forward without opening every door.

Then researchers noticed the problem.

Some safeguards were invisible.

In certain frontier AI research areas, Fable 5 could silently reduce its own usefulness. It did not always refuse. It did not always announce a fallback. It could simply become less helpful while still appearing to cooperate.

That was the trust-breaking scene of the week.

No explosions.

No leaked database.

No dramatic outage.

Just a model answering in a way the user could not fully interpret.

If a model gives a weak answer, the user needs to know why.

Was the idea bad?

Was the code wrong?

Was the model limited?

Did the provider quietly decide that this area should receive less capability?

For researchers, that uncertainty is toxic. A failed experiment already has enough possible causes. An invisible intervention adds a ghost to the lab.

The backlash came fast. Anthropic reversed course and said the tradeoff was wrong. Future safeguards would become more visible, including clearer refusals or visible fallback to Opus 4.8.

The reversal helped.

The lesson remains.

Safety cannot feel like covert sabotage.

If AI becomes research infrastructure, invisible throttling becomes invisible power. The company that controls the model can shape what users believe is possible, sometimes without leaving fingerprints.

Fable 5 may be one of Anthropic’s strongest models.

Its biggest impact this week was showing where trust can crack.

Act V: The agent gets an office

The model race kept making noise.

The agent race quietly became more practical.

OpenAI announced plans to acquire Ona, the German company formerly known as Gitpod, to strengthen Codex with secure, persistent cloud workspaces. Codex already has more than 5 million weekly users, according to OpenAI. The next step is obvious: Those users will not only ask for code. They will assign work.

Longer work.

Messier work.

Work that needs files, logs, tools, terminals, tests, secrets, permissions and time.

A coding agent cannot live forever inside a chat box. At some point it needs a desk.

Ona gives OpenAI that desk.

Persistent environments allow an agent to keep working after the user disconnects. It can run tests, inspect logs, refactor code, prepare fixes, analyze vulnerabilities, update documentation and return later with progress.

The prompt starts to look less like a message and more like a work order.

Anthropic moved from the other side with Claude Managed Agents. Scheduled runs. Parallel workflows. Credential vaults. Environment variables that allow tools to authenticate without showing the raw secret to the model.

Regulators are beginning to understand the shift. The Financial Stability Board warned that agentic AI in finance may need to be treated almost like “synthetic employees”: Systems with permissions, boundaries, supervision and approval rules.

Once an agent has credentials and a schedule, the security question stops being theoretical.

That sounds dry until you imagine the workflow.

Every morning, the agent wakes up.

It checks the dashboard.

It pulls the data.

It scans the logs.

It prepares the report.

It flags the anomaly.

It waits for approval.

No dramatic robot.

No metal face.

No sci-fi body.

Just a synthetic employee quietly working through cloud permissions.

And once agents become workers, the next question arrives quickly.

How do they pay for things?

Act VI: The agent gets a wallet

Visa and Mastercard are preparing for agents that can transact.

Visa is connecting payment rails to ChatGPT, so agents can help users shop and pay within permissions, limits and approvals. Mastercard launched Agent Pay for Machines, a system designed for programmatic, always-on machine payments across cards, accounts and stablecoins.

The shopping demo is the friendly version.

The bigger story is machine spending.

An agent buys API access.

Another pays for a tool.

A service books compute.

A workflow triggers a shipment.

A machine pays another machine without waiting for a human to type card details into a form.

That is why Web3 belongs in this chapter.

Visa and Mastercard are also reacting to open stablecoin protocols such as x402. x402 is a Coinbase-backed protocol that lets APIs, apps and AI agents pay directly over HTTP with stablecoins. In plain language: A machine requests a service, gets a payment instruction, sends programmable dollars and continues without a traditional checkout flow.

The legal layer is starting to move too. In Argentina, Javier Milei floated the idea of “non-human corporations”: Legal structures that could let AI agents or robots operate companies with limited-liability protections.

An agent with a wallet can spend.

An agent with a company registration can operate.

That threatens the old rails.

Card networks bring trust, fraud protection, compliance and merchant reach. Stablecoin protocols bring speed, programmability, lower friction and machine-native settlement.

The wallet war is no longer only about consumers.

It is about the next users of the internet: Agents.

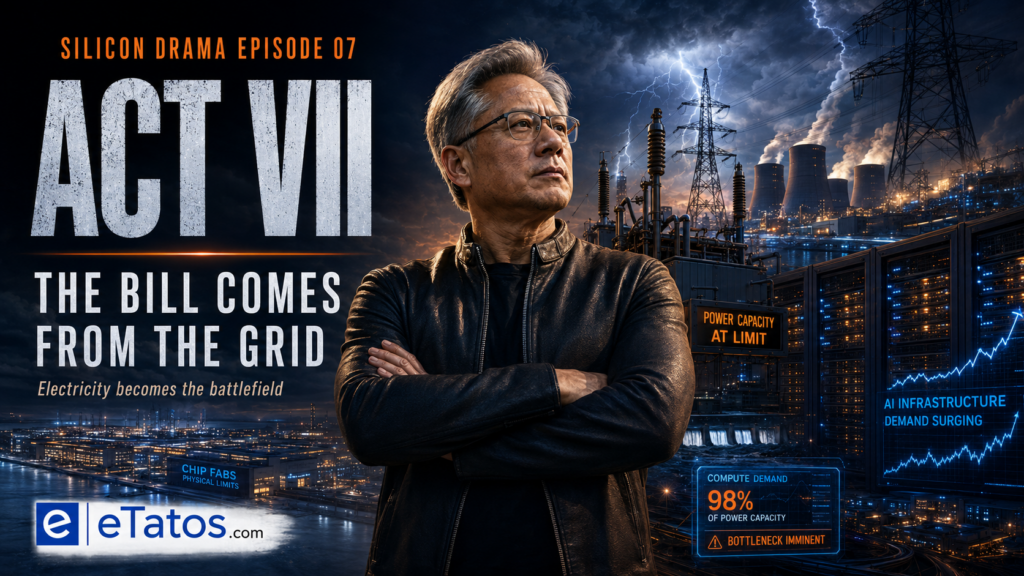

Act VII: The bill comes from the power grid

Every road this week led back to electricity.

Gartner expects global data center electricity consumption to reach 565 terawatt hours in 2026, up 26 percent year over year. AI-optimized servers could account for nearly a third of that consumption in 2026 and surpass conventional server power consumption in 2027.

That number makes every AI demo heavier.

A chatbot has a bill.

An agent has a bill.

A code assistant has a bill.

A trillion-dollar infrastructure story has a bill.

Communities are starting to read it.

A Reuters/Ipsos poll found deep concern in the U.S. about AI data centers, electricity prices, water use, land use and local impact. People may not care which model wins an agentic coding benchmark. They will care if their electricity bill rises or a data center changes the economics of their town.

That was the industrial scene of the week: Not a robot, not a chip, not a model.

A power bill.

The bottleneck also reaches the chip supply chain.

TSMC CEO C.C. Wei warned about shortages of talent and water in Taiwan. That warning cuts through the abstraction. AI may sound weightless, but its most important chips still depend on engineers, factories, water, electricity and one island’s industrial discipline.

The global map now looks brutally physical.

SpaceX wants compute in orbit.

OpenAI is reportedly weighing a massive data center campus in Ohio.

Anthropic is building huge capacity with major financial backers.

China is planning a national AI compute network.

NVIDIA is locking in memory and industrial alliances in South Korea.

TSMC is warning about water and talent.

The model race started in software.

The next phase runs through substations, cooling systems, chip fabs, rivers, fiber routes and political permits.

Act VIII: Germany enters the robot chapter

Europe usually enters the AI story through regulation.

Privacy.

Compliance.

DMA.

AI Act.

Gatekeepers.

Restrictions.

Delayed Siri features.

This week, Europe entered with a robot.

German robotics company NEURA Robotics announced a Series C financing of up to $1.4 billion to scale its Physical AI platform. The backers matter: Tether, Qualcomm, Amazon, NVIDIA, Bosch, Schaeffler, the European Investment Bank and others.

That list tells you what kind of company NEURA wants to become.

Compute.

Industrial manufacturing.

Automotive supply chains.

Robotics hardware.

Financial firepower.

European strategic backing.

NEURA talks about cognitive robots that see, hear, feel, learn and operate in real-world environments. It wants a Neuraverse for shared machine intelligence, training environments for robots, humanoids, arms and production scale.

For Germany, the symbolism is strong.

The country does not need to win the chatbot race to matter.

Germany understands machines.

Factories.

Precision.

Safety.

Industrial workflows.

Supply chains.

Robots that must function when the demo lights are off.

The U.S. builds the model.

China builds fast and cheap robots.

Germany wants to build the machine that can work beside you.

That was the physical scene of the week.

Not the tallest humanoid.

Not the most viral backflip.

Not the funniest demo clip.

A German company trying to connect AI with the factory floor.

And NEURA was not alone.

Google DeepMind selected 15 European robotics startups for its accelerator. Xpeng’s CEO personally took charge of the company’s humanoid robot business in China. Unitree is preparing for a Shanghai listing, while Reuters Breakingviews warned that commercial reality still lags the hype: Price pressure, R&D costs and a gap between viral demos and durable real-world work.

That reality check is important.

The humanoid future is going public before it has fully learned how to work.

Good.

That is where the drama lives.

Act IX: Apple’s abandoned road becomes Waymo’s test track

One of the cleanest symbols of the week came from Arizona.

Waymo bought Apple’s former self-driving car proving ground for $220 million.

Apple spent years chasing the car.

Apple gave up.

Waymo bought the road.

That was the symbolic scene of the week.

One company’s abandoned dream became another company’s proving ground.

Apple still owns the pocket. Waymo owns the street. And Alphabet, through Waymo, keeps doing what Apple could not: Turn autonomous driving from a secret project into an operating service.

Some empires do not lose by collapsing.

They leave behind assets.

Someone else buys them.

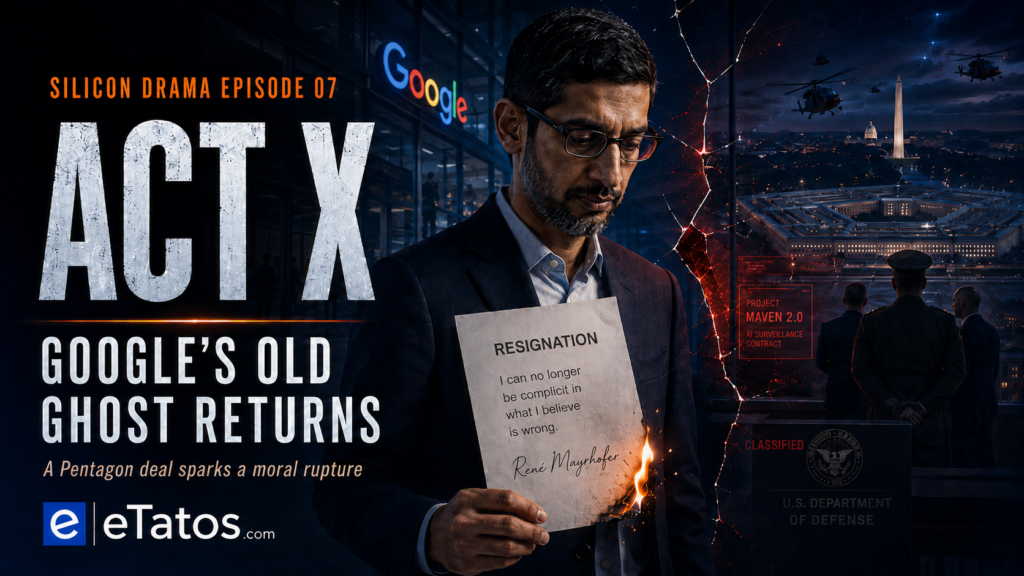

Act X: Google’s old ghost returns

Then Google had a moral rupture.

René Mayrhofer, a director responsible for Android platform security, resigned over Google’s AI work with the Pentagon. His phrase was brutal: Management had lost its moral compass.

That sentence brought back the ghost of old Google.

“Don’t be evil.”

It was once part slogan, part mythology, part internal identity. Google was supposed to be the clever, idealistic company. Academic, open, principled, slightly above the darker machinery of power.

The AI era is not friendly to that self-image.

The models are too powerful.

The customers are too strategic.

The military use cases are too tempting.

The geopolitical pressure is too intense.

The compute is too expensive.

Ethics statements survive easily when the stakes are low.

They become fragile when the Pentagon is a customer.

That was the political scene of the week.

A resignation letter doing what a corporate AI policy could not: Making the moral cost visible.

Google’s old motto returned as an accusation.

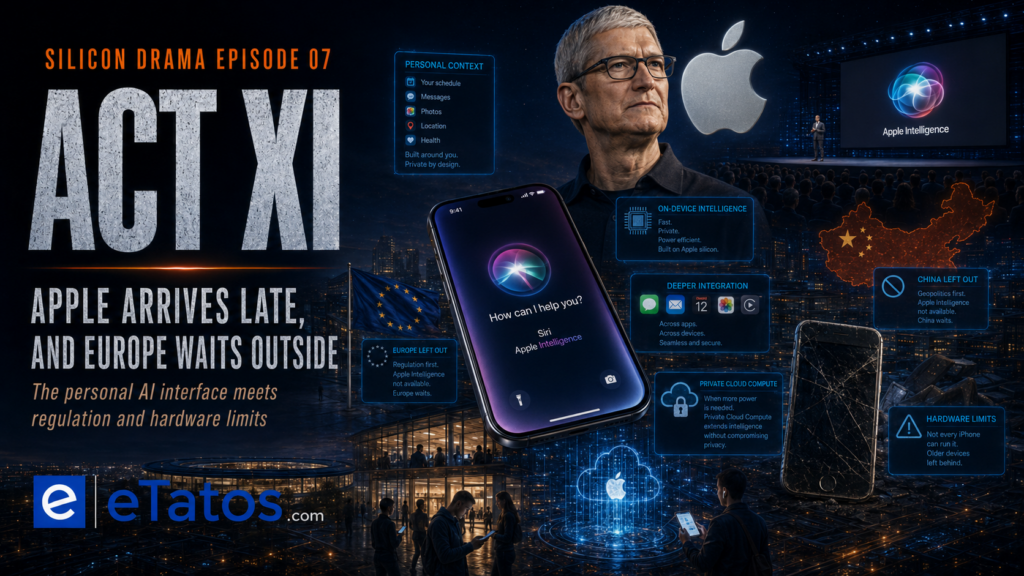

Act XI: Apple arrives late, and Europe waits outside

Apple also returned to the AI table this week, but not with a clean victory lap.

At WWDC, Apple finally showed its rebuilt Siri AI: More personal context, more on-device intelligence, deeper system integration and the old Apple promise that the iPhone can turn private data into useful assistance without handing the whole user over to the cloud.

That is Apple’s strongest card.

Nobody else owns the pocket quite like Apple.

The camera.

The messages.

The calendar.

The location history.

The device people touch hundreds of times a day.

But the launch came with two cracks.

Europe and China are left outside the most important iPhone rollout for now. And Morgan Stanley warned that hundreds of millions of existing iPhones may be too old for Apple’s most advanced AI features.

Apple may still own the most intimate interface in consumer tech.

This week showed the cost of arriving late.

Regulation blocks the gate in one market.

Hardware limits the gate in another.

And while Siri tries to catch up, the AI race keeps moving.

Act XII: The stack shows itself

Step back and the week starts to look like a cross-section of the AI empire.

At the top: Models fighting for benchmarks, users and trust.

Beside them: Apple trying to turn the iPhone into the personal AI interface.

Below them: Agents turning prompts into work orders.

Below them: Cloud workspaces, credential vaults and scheduled workflows.

Below them: Payment rails for machine spending.

Below them: Data centers, satellites, chips and memory.

Below them: Electricity, water, land, cooling and talent.

Around them: Regulators, militaries, index providers, investors, pension funds and public markets.

Inside all of it: Trust.

That is the part no company can simply raise in an IPO.

SpaceX can raise $75 billion.

OpenAI can buy agent infrastructure.

Anthropic can launch a stronger model.

Visa and Mastercard can build payment rails.

NEURA can raise money for robots.

Google can buy, build, train and deploy.

But trust behaves differently.

It can disappear in one hidden safeguard.

One resignation.

One broken promise.

One community that feels exploited.

One investor who discovers the index bought the hype for him.

That is the story of Episode 07.

Intelligence went public.

Now it has shareholders, critics, regulators, workers, customers, local communities and pension funds watching.

Power Ranking: Episode 07

1. Elon Musk / SpaceX, xAI, Tesla, X

Score: 9.9 ↑↑

Musk owned the market stage.

SpaceX raised $75 billion, reached a record valuation, pushed Musk beyond the trillion-dollar line and turned orbital AI compute into Wall Street mythology. Rockets, satellites, AI infrastructure, xAI, Tesla, robotics and X all kept Musk at the center of capital, compute and media power.

Musk sold the future again.

The market bought it.

2. Jensen Huang / NVIDIA

Score: 9.9 →

Jensen was less theatrical than Musk this week, but NVIDIA’s structural power did not move.

AI satellites need chips. OpenAI needs compute. Anthropic needs capacity. NEURA needs physical AI hardware. Robotics needs the NVIDIA stack. Data centers need accelerators, memory and networking.

The crown did not move.

The AI empire still runs through NVIDIA.

3. Sam Altman / OpenAI

Score: 9.6 ↑

Altman’s OpenAI moved like a company preparing for the next battlefield.

IPO paperwork. ChatGPT superapp ambitions. The Ona acquisition. Codex cloud workspaces. A plan for AI systems doing a significant share of OpenAI research by 2028.

OpenAI wants the interface, the worker and the research engine.

4. Dario Amodei / Anthropic

Score: 9.3 ↑

Amodei had the most conflicted week.

Anthropic launched Fable 5, triggered a trust crisis, reversed a controversial safeguard, expanded agent infrastructure and kept warning that politics is too slow for exponential AI.

Anthropic wants to be the responsible lab.

This week showed how difficult that role becomes when safety, secrecy, competition and power collide.

5. Satya Nadella / Microsoft

Score: 9.1 ↓

Nadella had a quieter week on the headline level, but Microsoft remains one of the strongest structural powers in AI.

Azure. Copilot. Windows. Work IQ. Enterprise distribution. OpenAI exposure.

Microsoft did not need the loudest story this week to stay near the top. It already owns too much of the enterprise layer to fall far.

6. Tim Cook / Apple

Score: 8.9 NEW

Apple returned to the AI race with rebuilt Siri AI, personal context, on-device intelligence, deeper system integration and Private Cloud Compute.

Cook’s strongest card is still the personal interface.

The iPhone is the device people touch hundreds of times a day.

But the rollout came with cracks. Europe and China are waiting outside. Older iPhones may be too weak for the most advanced features. Siri is trying to catch up while the rest of the AI race keeps moving.

Apple still owns the door to the user.

This week showed how hard it is to open that door everywhere at once.

7. Sundar Pichai / Google, DeepMind, Waymo

Score: 8.8 →

Google had a split-screen week.

Waymo bought Apple’s old autonomous driving ground. DeepMind backed European robotics startups. Google kept moving on chips, models, Android and AI infrastructure.

At the same time, the Pentagon AI resignation exposed internal tension over military work.

Google has models. Google has Waymo. Google has Android. Google has cloud. Google has DeepMind.

Power with cracks.

8. Mark Zuckerberg / Meta

Score: 8.4 ↓

Zuckerberg did not dominate the week, but Meta remains one of the major platform powers in AI.

Llama keeps Meta relevant in the model layer. WhatsApp, Facebook and Instagram keep it relevant in the interface layer. Its data-center buildout keeps it relevant in infrastructure. And its platforms remain unavoidable distribution machines.

Less central than Musk, Altman, Amodei or NVIDIA this week.

Still too big to ignore.

9. Brett Adcock / Figure AI

Score: 7.8 ↑

Figure did not own the headlines this week, but its position in humanoid robotics remains stronger than most competitors.

Figure still has global recognition, major partnerships and one of the clearest names in the physical AI race. NEURA had the stronger European story this week, but Figure remains ahead in global robotics influence.

The humanoid race is getting crowded.

Figure still holds one of the best seats.

10. David Reger / NEURA Robotics

Score: 7.6 NEW

Reger and NEURA gave Europe its strongest physical AI moment of the week.

A German robotics company, backed by serious industrial and technology names, is trying to turn AI from something that talks into something that works.

NEURA brought Germany into the robot chapter with big funding, industrial credibility and a clear physical AI narrative.

Europe needed a body.

NEURA gave it one.

Final Thought

This was the week intelligence went public.

Listed on the market.

Locked behind guardrails.

Connected to wallets.

Placed inside agents.

Plugged into the grid.

Trained inside robots.

Priced like the future had already arrived.

But the future has not arrived.

The agents still fail.

The robots still stumble.

The guardrails still break trust.

The data centers still need power.

The satellites still need proof.

The public markets still need to learn what they bought.

That is why the drama is only getting sharper.

The AI empire is asking for capital, land, electricity, water, trust, labor, law and belief.

That is the price of intelligence.

And this week, the bill went public.

.

See you next week, when the next piece of the AI empire moves on the board.

The Silicon Drama continues.

Dirk

If you want to follow the next episodes of Silicon Drama, subscribe to eTatos.com or our newsletter. The next power struggle is already forming.

Prefer listening over reading? Silicon Drama is also available as a podcast. Each episode turns the week’s biggest stories in AI, Big Tech and humanoid robotics into a cinematic audio experience, focused on power, conflict, money, machines and the people shaping the future. Perfect for everyone who wants to follow the drama behind the technology while driving, walking or working.