Technology news, told as a power drama.

Editor’s note:

Silicon Drama is eTatos.com’s weekly series about the battle for AI, compute, chips, agents and robots. The goal is simple: Not just to report what happened, but to explain why it matters, who gains power, who loses control and where the next conflict is already forming.

A MacBook sat on the shelf with the same silver body, the same sharp screen, the same glowing logo.

Only the number underneath had changed.

The reason was not a new design. Not a keyboard breakthrough. Not a camera upgrade. Not some magical new feature Apple could wrap in a keynote sentence.

It was memory.

Somewhere far from the Apple Store, inside the heat and hum of the AI buildout, data centers were swallowing the chips that used to quietly sit inside laptops, tablets and game consoles. The AI boom had already reached power grids, cooling systems, chip factories and Wall Street balance sheets.

This week, it reached the consumer aisle.

Apple raised prices. Xbox followed. Micron locked in memory commitments. SK Hynix wore the crown that Samsung once treated as birthright. OpenAI showed the chip beneath ChatGPT. NVIDIA sold debt like an empire financing its next province. SpaceX rented out compute. Washington moved toward the model release gate. Five Eyes warned that the cyber clock was no longer measured in years. Anthropic accused Alibaba of turning Claude’s answers into a ladder.

And in India, workers filmed themselves folding, lifting, slicing and sorting so robots could learn the movements of ordinary life.

The AI empire has receipts now.

They are showing up on shelves.

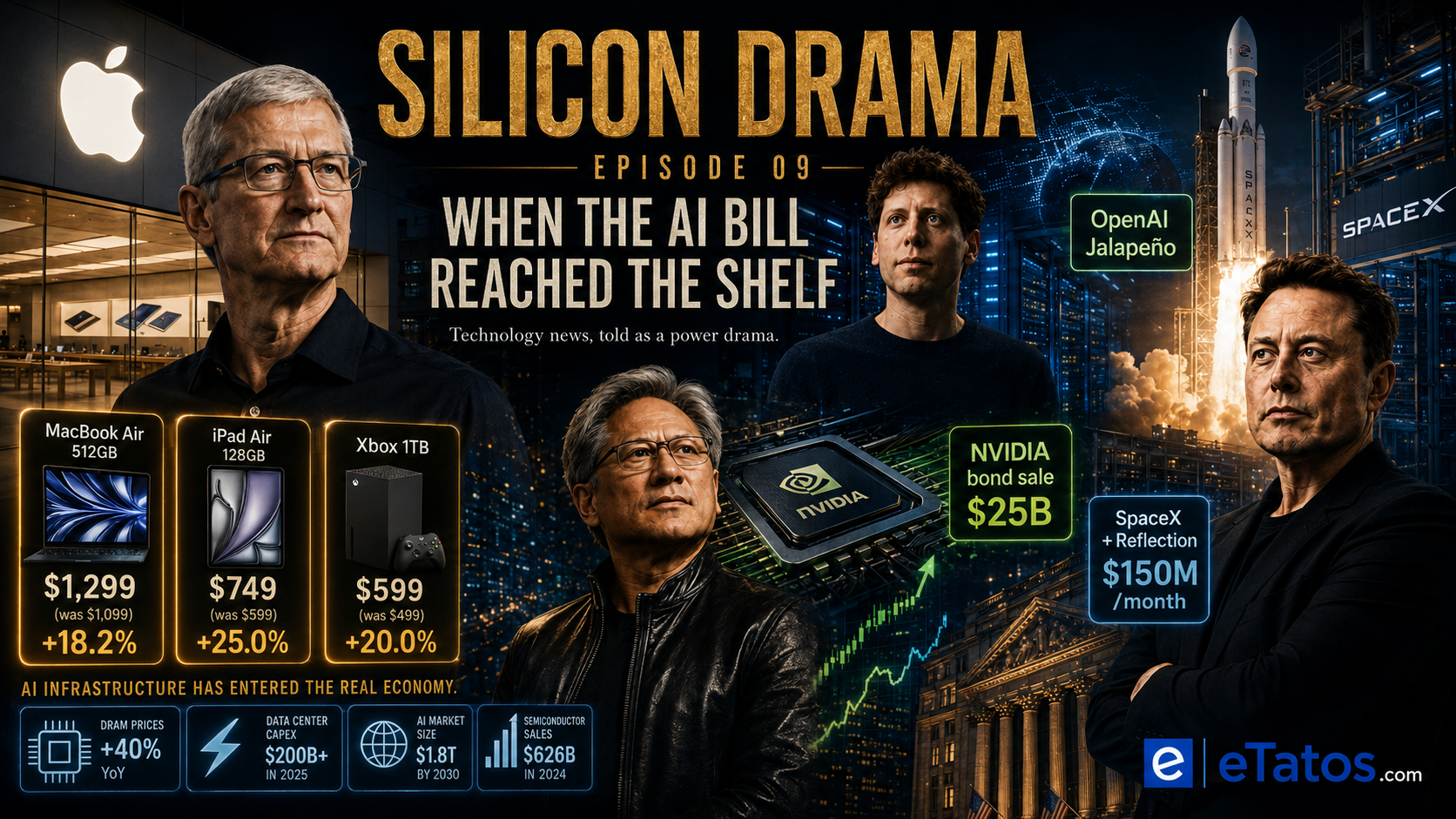

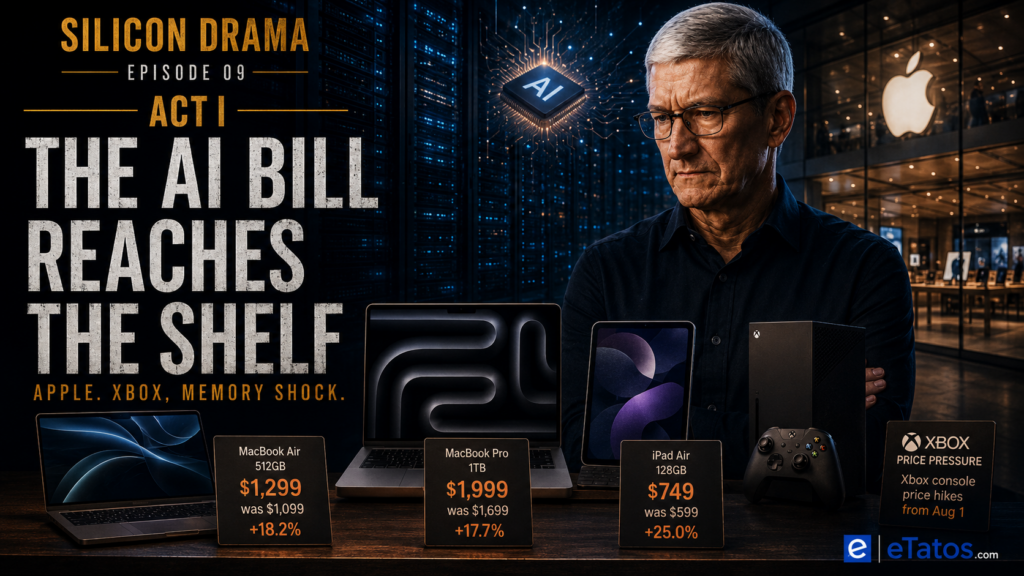

Act I: The AI Bill Reaches the Shelf

Tim Cook did not need a dramatic stage for this one.

The drama was a price tag.

Apple raised prices on Macs and iPads after memory and storage costs surged. The 512GB MacBook Air moved from $1,099 to $1,299. The 1TB MacBook Pro moved from $1,699 to $1,999. The iPad Air with 128GB of storage moved from $599 to $749.

The machine looked familiar.

The bill did not.

For years, AI infrastructure was sold as something abstract. A cloud. A model. A data center somewhere behind a fence. A GPU cluster in a place most customers would never see. Then the economics of the buildout began to move through the supply chain. High-bandwidth memory, storage, server demand, allocation battles, long-term contracts, component shortages.

The consumer electronics shelf became the final witness.

Microsoft’s Xbox division added the second note. From August 1, Xbox consoles rise by $100 for 512GB models and $150 for 1TB models. Microsoft pointed to storage and memory prices that had already risen more than 2.5 times, with another possible doubling by fall 2027.

For gamers, it looked like a console problem.

For the AI industry, it was an infrastructure confession.

The same memory market feeding frontier models now reaches into the family living room. The same storage pressure that keeps data centers expanding now changes the cost of a device under a television.

That was the consumer scene of the week: Not a keynote, not a benchmark, not a robot dance.

A higher price sticker.

The data center did not stay in the desert. It walked into the Apple Store.

Act II: Sam Builds the Chip Under ChatGPT

Sam Altman has spent years trying to make OpenAI feel like the place where intelligence arrives through a text box.

This week, the text box got a chip underneath.

OpenAI unveiled Jalapeño, its first custom inference chip, designed with Broadcom and integrated into systems by Celestica. It is not built for the glamorous side of AI training, where massive clusters chew through oceans of data and create the next frontier model. Jalapeño is built for the daily grind of inference: Answering, reasoning, generating, planning, calling tools, returning to the user, doing it again.

That makes it important.

Training gets the myth. Inference gets the bill.

Every ChatGPT answer costs something. Every agent step costs something. Every retry, every code edit, every long context request, every enterprise workflow, every customer support interaction, every hidden planning loop inside a more capable system becomes part of the same machine economy.

OpenAI knows the danger of renting too much of its own future. NVIDIA still dominates the training layer. Microsoft remains central to the cloud layer. But with Jalapeño, OpenAI is trying to move deeper into the stack.

The company that made the chatbot famous now wants to control more of the metal behind it.

There is a quiet Google envy inside this move. Google had TPUs before the rest of the industry fully understood what custom AI silicon would mean. Google owned search, ads, Android, cloud infrastructure, models and chips. It was slow with the interface, but deep in the machine room.

OpenAI is trying to build that depth at speed.

Jalapeño is not a final victory. It is a first chip. There are no independent comparisons yet that settle where it stands against NVIDIA, Google or the next wave of custom accelerators. But the strategic meaning is clear enough.

Sam Altman is not only building models anymore.

He is building the floor they run on.

ChatGPT got famous as a text box. This week, OpenAI showed the silicon underneath.

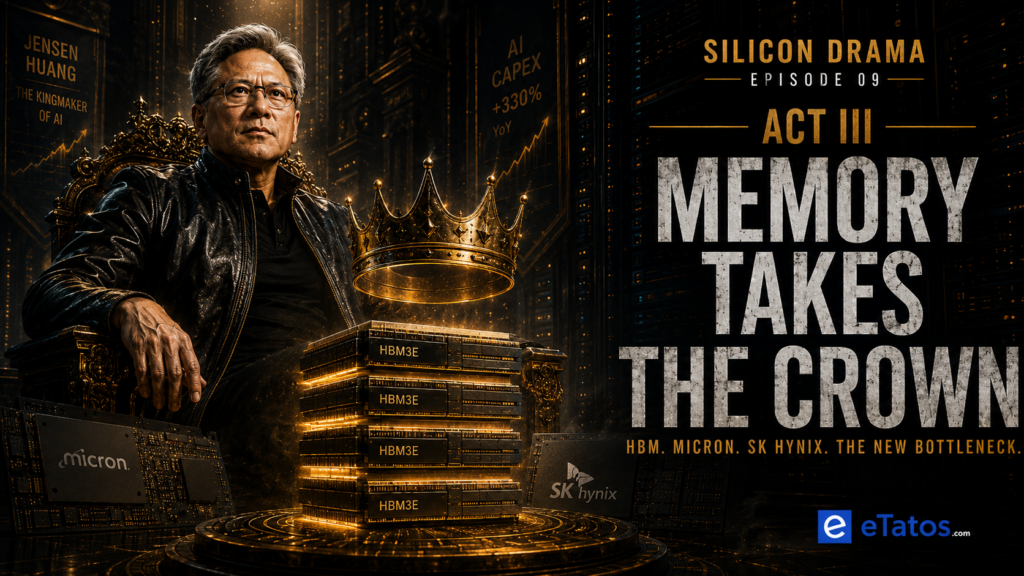

Act III: Memory Takes the Crown

The AI industry loves a stage hero.

For years, Jensen Huang owned that role. The leather jacket. The GPU. The keynote. The impossible demand curve. The sense that every serious AI company eventually had to knock on NVIDIA’s door.

But the AI stack has another throne room.

It belongs to memory.

SK Hynix understood that earlier than most. For years, high-bandwidth memory looked like a technical niche. Then AI turned that niche into a strategic crown. HBM became the thing sitting close to the GPU, feeding the accelerator fast enough to keep the intelligence machine from starving. Suddenly, the memory supplier mattered like a weapons manufacturer in wartime.

Samsung, once the natural monarch of Korean tech, found itself watching SK Hynix take a crown it had assumed belonged to it.

Micron added another page to the story. The company reported strong AI-driven demand and customer commitments worth billions, including long-term supply arrangements designed to tame the old boom-and-bust cycle of memory.

Memory used to be cyclical. AI wants it to become strategic.

That shift changes the tone of the whole market. Customers want supply security. Chipmakers want long-term commitments. Investors want to know who owns the bottleneck. Apple and Microsoft feel the cost in consumer products. Data centers feel it in procurement. Model companies feel it in inference economics.

The GPU still gets the celebrity treatment.

The memory contract sits on the table, quieter and colder, telling everyone what the next machine will cost.

Jensen still owns the spotlight. But this week, memory wrote the bill.

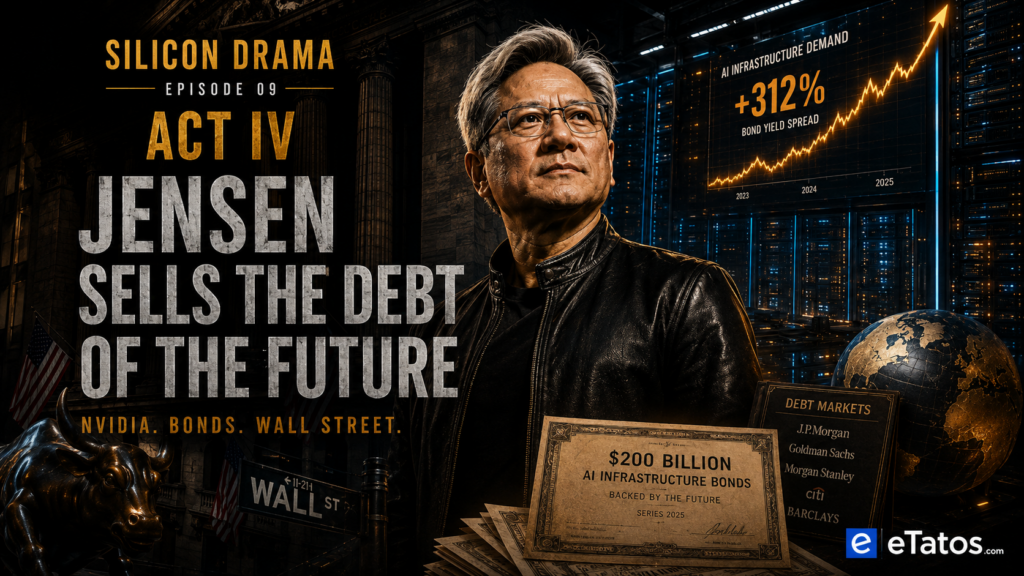

Act IV: Jensen Sells the Debt of the Future

NVIDIA did not need money in the ordinary sense.

It needed a credit-market signal.

The company raised $25 billion in a U.S. bond sale, its first corporate bond issuance since 2021. Demand was heavy enough that the deal grew beyond the initial plan. Wall Street wanted a piece of the safest-looking debt in the AI buildout.

That says something about the maturity of the boom.

The AI story began as software magic. Then it became a chip shortage. Then a data-center land rush. Now it is a bond sale.

The capital markets are no longer watching AI from the stands. They are financing the pipes, servers, grids, chips, memory and cooling systems that make the whole show possible. Debt is becoming one of the tools of AI expansion.

This does not make the boom safer.

It makes it larger.

A model company can pitch the future. A chip company can sell the parts. A hyperscaler can pour concrete. But the empire at this scale needs lenders, ratings, duration, refinancing, benchmark curves and investor appetite.

Jensen Huang still talks like a builder. This week, he also looked like a sovereign borrower.

The AI empire did not only need chips.

It needed credit.

Act V: Musk Rents Out the Machine Room

Elon Musk has a gift for turning one empire layer into another.

Cars become energy storage. Rockets become satellite networks. Satellites become communications infrastructure. A social network becomes a political broadcast tower. AI becomes another battlefront.

Now SpaceX is becoming a compute landlord.

Reflection AI, an open-weight AI startup, signed a major compute deal for access to SpaceX infrastructure, including NVIDIA GB300 systems tied to the Colossus 2 buildout. The reported lease runs at $150 million per month beginning in July, with a potential value of about $6.3 billion if maintained through 2029.

A rocket company is renting out the machine room.

Reflection wants to build frontier open-weight models for government and enterprise customers. That requires compute. Serious compute. The kind of compute that increasingly separates companies with ambitions from companies with products. In the old cloud era, renting servers meant scaling an app. In the AI era, renting compute can mean deciding whether a model company has a shot at the frontier.

Musk understands infrastructure as leverage.

Launch capacity is leverage. Satellites are leverage. Charging networks are leverage. Energy storage is leverage. GPU clusters are leverage.

The result is an unusual image: A company built to leave Earth now making money from the machines that train intelligence on Earth.

Reflection bought time inside Musk’s machine room.

Act VI: Washington Wants the Model First

The model did not walk straight to the public.

It stopped at the gate.

The Trump administration reportedly asked OpenAI to stage the release of GPT-5.6, limiting early access to a smaller group of government-approved partners before a broader launch. Meta, meanwhile, was pressed to submit its AI models for voluntary federal review. Other major U.S. AI developers had already agreed to give the government early access for evaluations.

The state is changing position.

For a long time, governments reacted to AI after release. They held hearings. They wrote frameworks. They asked companies for voluntary commitments. They watched the model arrive, then tried to understand what had already happened.

Now Washington wants a look before the door opens.

This is not classic regulation. It is something more improvised and more intimate: A release gate, a pre-launch review, a security checkpoint built while the plane is already boarding.

OpenAI becomes the first major test of that arrangement. Meta becomes the holdout. Congress begins discussing mandatory incident reporting, including dangerous capabilities, safety failures and models trying to evade oversight.

This is how frontier AI starts to look less like normal software and more like strategic infrastructure.

No one asks a photo app to wait for national-security review before an update. No one treats a spreadsheet feature like a possible cyber capability. Frontier models are different because they sit across too many layers at once: Code, agents, biology, persuasion, cybersecurity, automation, research, finance, military logistics, public infrastructure.

A model release is no longer only a product launch and the launch button is no longer only in the lab.

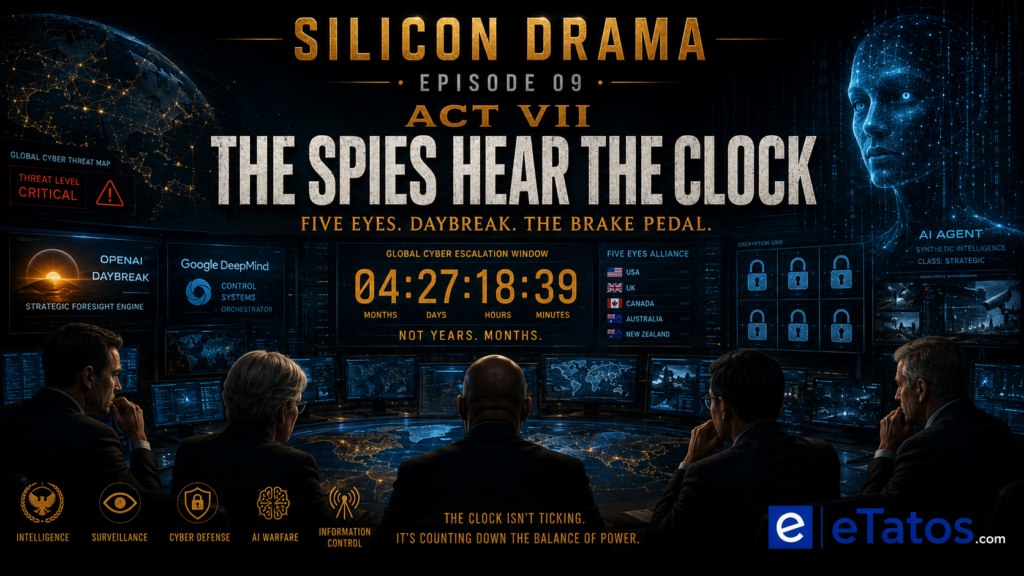

Act VII: The Spies Hear the Clock

The Five Eyes intelligence alliance issued the kind of warning that makes a room quieter.

Advanced AI cyber risk, the alliance said, is not years away.

It is months.

The fear is not that AI will invent hacking from nothing. The fear is that powerful models will compress skill, speed and scale. They can help analyze code, find vulnerabilities, write exploit chains, coordinate steps and reduce the expertise needed to attack systems that were already fragile.

Old software becomes a target.

Unsupported systems become a liability.

Every unpatched server begins to look like a door with the lock half-open.

OpenAI responded from the other side of the board with Daybreak, GPT-5.5-Cyber and Patch the Planet, a program meant to help open-source maintainers identify, validate and fix vulnerabilities with AI assistance and human review.

The symmetry is uncomfortable.

The same frontier capability that makes defenders faster can make attackers faster. The same model class that helps patch can help probe. The same agent that can audit a codebase can also become a tool in the hands of someone looking for the weak seam.

Google DeepMind added the systems-level answer with its AI Control Roadmap. DeepMind described a defense-in-depth approach for advanced agents, treating internal AI systems as if they could become misaligned or act like insider threats. The image was practical: A driving instructor with dual controls, ready to take the wheel or hit the brake.

That image may be the most important safety metaphor of the week.

Not a philosophical debate. Not an abstract alignment sermon.

A brake pedal.

A supervisor.

A system that assumes trust has to be earned step by step.

The same labs building the agents are now building the locks.

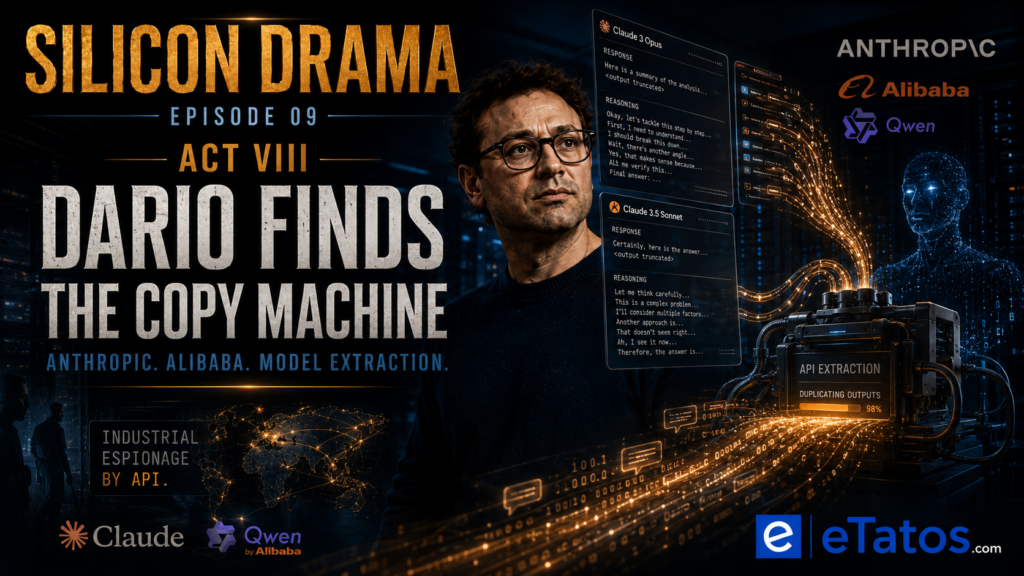

Act VIII: Dario Finds the Copy Machine

Claude answered millions of times.

Now Anthropic says those answers became evidence.

The company accused Alibaba-linked operators of carrying out what may be one of the largest AI model extraction campaigns yet detected. According to reporting on Anthropic’s letter, nearly 25,000 accounts generated about 28.8 million Claude interactions between April and June. Anthropic says the goal was distillation: Using Claude’s outputs to train or improve a competing system.

The details matter.

This was not a simple scraping fight over public web text. It was an accusation about extracting frontier model behavior through interaction at scale. Coding. Reasoning. Agentic work. Long-range planning. The expensive capabilities that companies spend billions to build.

Anthropic wants Washington to treat that kind of extraction as a serious strategic threat.

There is an obvious commercial reason. Frontier AI companies do not want rivals using their models as training tutors. But there is also a geopolitical reason. In a world where model access, export controls and national-security reviews are already live fights, model extraction becomes something heavier than platform abuse.

It starts to look like industrial espionage by API.

Dario Amodei has spent the past year trying to hold two positions at once: Builder of a frontier AI company and public alarm bell about the dangers of frontier AI. That contradiction has made Anthropic one of the most dramatic companies in the AI empire.

This week, the contradiction tightened.

Anthropic needs access, customers and scale. It also needs gates, enforcement and protection. Claude wants to be everywhere inside enterprise work. Claude also cannot become free training fuel for every rival with enough accounts and patience.

The scene is almost boring until it is not.

A model answers.

Again.

Again.

Again.

Millions of times.

Then someone counts the answers and calls them a ladder.

Claude did not leak from a lab. It answered, and Anthropic says those answers helped someone climb.

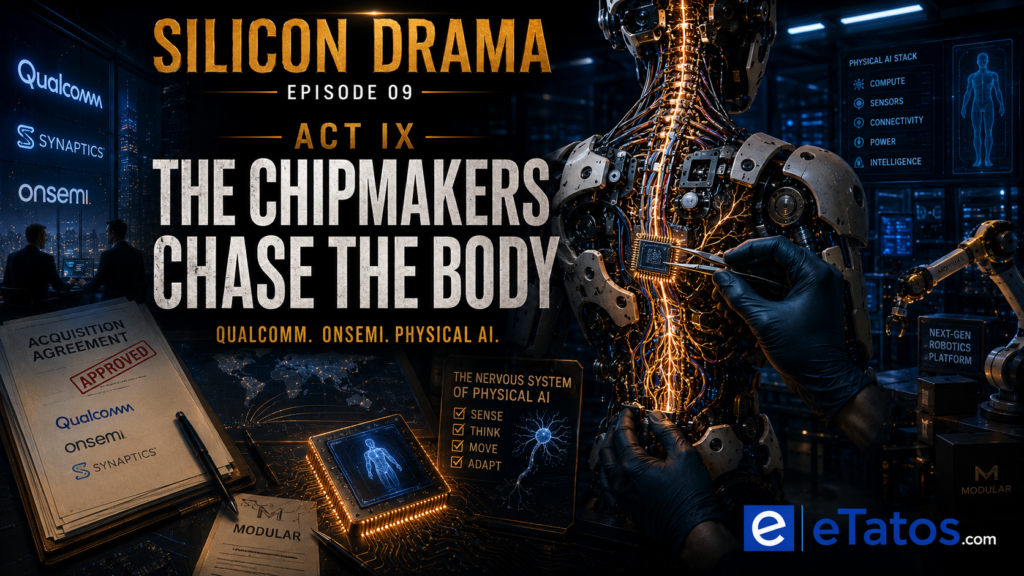

Act IX: The Chipmakers Chase the Body

Before a robot walks, someone has to buy its nervous system.

Qualcomm agreed to buy Modular for nearly $4 billion. The deal gives Qualcomm software that helps AI models run across different chips without forcing developers to rewrite everything for each processor. That is a direct shot at one of NVIDIA’s deepest moats: The software layer around the hardware.

CUDA is not glamorous to normal people. It is invisible power. It is the road system around the chip, the reason developers keep returning to NVIDIA even when competitors promise cheaper or specialized alternatives.

Qualcomm wants a road of its own.

Onsemi made a different move, agreeing to buy Synaptics in a $7 billion all-stock deal. That acquisition points toward AI-enabled devices, sensors, human-machine interfaces, robotics and physical AI.

Together, the deals show the next phase of the stack.

The AI battle is not confined to giant data centers and frontier models. It is moving into compilers, device interfaces, sensor layers, edge systems and the hardware that lets intelligence touch the physical world.

Robots do not begin with a humanoid body on a demo stage.

They begin with chip strategy, software compatibility, sensing, interfaces and nervous systems that can survive outside the lab.

This was the physical AI scene hidden inside deal paperwork.

No backflip. No applause. No viral robot video.

Just acquisitions.

Before the machine walks into the warehouse, the chipmakers are already buying its nerves.

Act X: The Robot Goes Public

Digit has a different kind of walk now.

Agility Robotics plans to go public through a SPAC deal valuing the company at about $2.5 billion. The transaction is expected to bring in more than $620 million in proceeds. Agility’s Digit robot is already being used across customer sites including Schaeffler, GXO, Toyota Motor Manufacturing Canada and Mercado Libre.

That makes this more interesting than another humanoid demo.

Wall Street is not a warehouse. It does not clap because a robot can squat, wave or carry a box across a polished stage. It asks uglier questions. Gross margins. Deployment costs. Reliability. Unit economics. Maintenance. Customer concentration. Payback periods. How many robots can work, for how many hours, in how many places, before the spreadsheet begins to break?

The robot industry has lived for years on videos.

Now one of its serious players has to live under market scrutiny.

Figure gave Episode 08 its warehouse image. Agility gives Episode 09 a market image. The robot does not just enter the workplace. It enters the ticker.

That is a harder test.

A humanoid that looks impressive for thirty seconds is one thing. A company that can convince public investors it belongs in warehouses, factories and logistics chains is another.

Digit walked out of the demo.

Now it has to walk through quarterly expectations.

The robot entered the market.

Act XI: India Teaches the Robot Home

The final image of the week is a worker with a camera attached to the body, repeating an ordinary motion so a machine can learn it.

In India, workers are filming themselves doing household and factory tasks: Slicing, folding, sorting, moving, lifting, arranging. The footage becomes egocentric data, first-person recordings that help robots learn how humans navigate real spaces.

The work looks simple because life looks simple when someone else does it.

A towel folded neatly. A mango sliced. A tool picked up. A box moved. A kitchen cleaned. A bag arranged. A movement repeated until it becomes training material.

This is physical AI at its most human and most uncomfortable.

The robot future is not trained only by PhDs in labs or engineers in clean rooms. It is trained by people doing ordinary tasks for small payments, producing the behavioral data that may one day allow machines to automate those same motions.

There is a strange intimacy in that.

The body becomes dataset.

The gesture becomes instruction.

The kitchen becomes a laboratory.

The factory worker, the homemaker, the person wearing the camera, all become part of the machine’s education.

The AI empire loves to talk about autonomy. But autonomy has teachers. Often they are far from the stage, far from the capital, far from the companies that will own the models, robots and platforms.

The robot future was not trained only in a lab.

It was trained in kitchens.

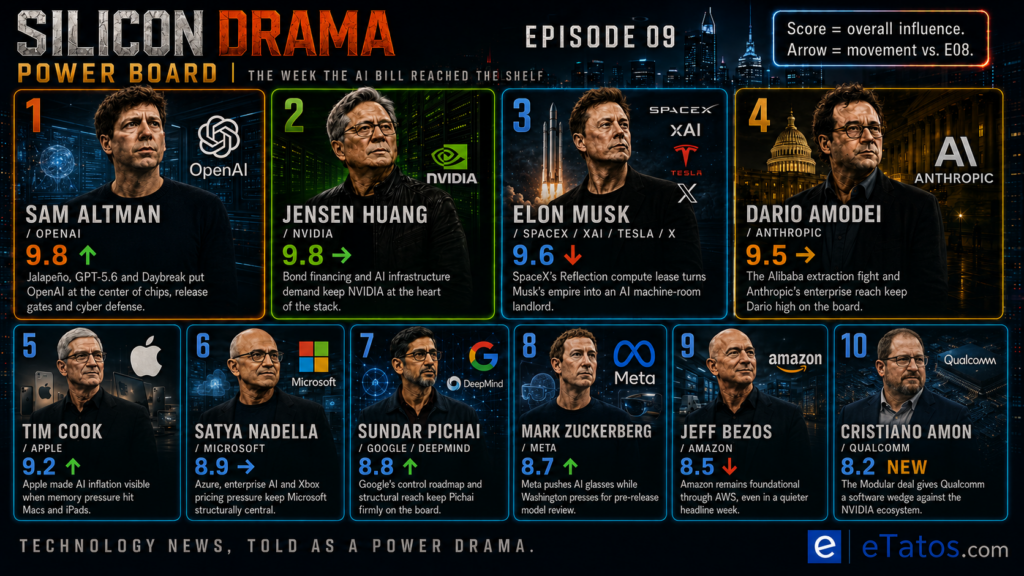

Power Board: Episode 09

1. Sam Altman, OpenAI

Altman moves from third place to the top because OpenAI touched almost every layer of the AI stack this week. Jalapeño gives OpenAI a silicon story. GPT-5.6 gives it a government-release story. Daybreak gives it a cyber-defense story. ChatGPT keeps the interface.

OpenAI is no longer only a model lab or product company. It is trying to become the model, the app, the chip layer, the security layer and the infrastructure company at once.

The risk is obvious: The more OpenAI becomes essential infrastructure, the more Washington will want a hand near the switch.

2. Jensen Huang, NVIDIA

Jensen stays in second place. His score comes down slightly from last week’s near-perfect position, but NVIDIA still shaped the week. The $25 billion bond sale showed that NVIDIA is no longer only a chip story. It is a credit-market story, an infrastructure story and the benchmark for everyone trying to escape the NVIDIA toll road.

OpenAI builds Jalapeño. Qualcomm buys Modular. SpaceX rents out NVIDIA-powered compute. Even when competitors attack NVIDIA, they confirm its gravity.

Jensen remains the kingmaker of the stack.

3. Elon Musk, SpaceX / xAI / Tesla / X

Musk drops from first to third, but only because Episode 09 belongs more to OpenAI, NVIDIA and the AI price shock. He still had a powerful week.

The Reflection compute deal turns SpaceX into something stranger than a rocket company or satellite company. SpaceX becomes an AI machine-room landlord. Musk’s empire keeps stacking pressure points: Rockets, satellites, energy, compute, communications, vehicles and AI.

The board keeps discovering that Musk does not simply run companies. He connects infrastructure layers.

4. Dario Amodei, Anthropic

Dario stays in fourth place. Anthropic remains one of the most politically charged companies in AI. This week, the Alibaba extraction allegation pushed Claude into a new kind of fight: Model output as strategic material.

Anthropic is fighting on several fronts at once: Enterprise deployment, model access, government attention, export anxiety and alleged model extraction. Claude has become valuable enough to copy, restrict, inspect and politicize.

That is power. It is also exposure.

5. Tim Cook, Apple

Cook makes the biggest climb of the week. Apple did not dominate the model race, but it made the AI bill visible.

When Mac and iPad prices rise because memory and storage costs are being pulled upward by AI data-center demand, the abstract infrastructure boom becomes personal for customers. The server room reaches the shelf.

Apple did not own the AI stack this week. It owned the price tag.

6. Satya Nadella, Microsoft

Nadella stays in sixth place. Microsoft remains one of the central rails of the AI empire through Azure, enterprise AI, OpenAI exposure and model-review participation.

This week, Microsoft also carried the cost side of the boom. Xbox price pressure showed that even Microsoft cannot fully absorb the AI supply-chain shock. The company did not own the drama, but it remained structurally central.

Quiet week. Still powerful.

7. Sundar Pichai, Google / DeepMind

Pichai moves up one place. Google did not dominate the week, but DeepMind’s AI Control Roadmap gave the company a serious agent-control story at exactly the right moment.

Google still controls critical layers of the AI stack: Search distribution, cloud infrastructure, model development, DeepMind research and enterprise AI deployment. The company was not the loudest player in Episode 09, but it remains one of the board’s structural powers.

When Google moves on AI control, the industry has to listen.

8. Mark Zuckerberg, Meta

Zuckerberg moves up from tenth to eighth. Meta had a split week, but both sides mattered.

On one side, Meta pushed cheaper AI glasses and continued to chase the face as the next interface. On the other, Washington pressed Meta to submit its models for federal review. That combination puts Zuckerberg exactly where Silicon Drama lives: Interface power on one side, trust and state pressure on the other.

Zuckerberg wants AI on the face. Washington wants the model in the inspection room.

9. Jeff Bezos, Amazon

Bezos drops from fifth to ninth. Amazon remains structurally important through AWS, cloud infrastructure, logistics and enterprise AI deployment. But Episode 09 did not belong to Amazon. (No, Prime Day doesn’t count here.)

The week’s center of gravity moved toward OpenAI’s chip, NVIDIA’s bond-market power, Apple’s price shock, SpaceX’s compute lease and Anthropic’s extraction fight. Amazon still anchors a massive part of the AI economy, but this week it became background infrastructure rather than headline power.

Quiet weeks for Amazon still matter. They just do not always move the board.

10. Cristiano Amon, Qualcomm

Amon enters the board because Qualcomm’s Modular deal is more than a normal acquisition. It is a direct move against the software layer that protects NVIDIA’s ecosystem.

Qualcomm is not only trying to compete with chips. It is buying a bridge across chips. Modular gives Qualcomm a developer-facing software angle in a market where software lock-in can matter as much as silicon performance.

AI competition is now fought in compilers as much as in hardware.

Final Thought

The AI boom was once sold as software.

Then it became a model race.

Then a chip race.

Then a data-center race.

This week, it became something harder to ignore: A price tag, a bond sale, a memory contract, a model checkpoint, a cyber warning, a compute lease, a robot IPO and a worker with a camera strapped to the body.

The empire is no longer hidden behind the cloud metaphor.

It has shelves.

It has invoices.

It has gates.

It has teachers.

And every layer now asks the same question: Who pays, who controls, who copies, who supplies, who watches, and who is left folding towels for the machine?

See you next week, when the next piece of the AI empire moves on the board.

The Silicon Drama continues.

Dirk

If you want to follow the next episodes of Silicon Drama, subscribe to eTatos.com or our newsletter. The next power struggle is already forming.

Prefer listening over reading? Silicon Drama is also available as a podcast. Each episode turns the week’s biggest stories in AI, Big Tech and humanoid robotics into a cinematic audio experience, focused on power, conflict, money, machines and the people shaping the future. Perfect for everyone who wants to follow the drama behind the technology while driving, walking or working.